Eric Sepanek

SBC Founder

Eric Sepanek is the founder of Scottsdale Bullion & Coin, established in 2011. With extensive experience in the precious metals industry, he is dedicated to educating Americans on the wealth preservation power of gold and silver.

Going to college, getting married, and buying a house has defined the American Dream for decades—but it’s slipping out of reach for younger generations.

In an increasingly competitive, globalized economy, entering the job market requires a college degree, and it comes at a steep cost: $1.5 trillion in student loan debt. That’s more than twice as high as it was in 2008.

The return on that massive investment is diminishing. With earnings flat for the last 50 years and studies showing that the country’s largest generation, Millennials, is “losing its edge against international peers,” the odds are stacked against young Americans AND THE NATION.[1]

When consumer spending nosedives so does the GDP and, in turn, the dollar.[2][3] Factor in rising interest rates and job automation, and the outlook for America’s long reign as world superpower looks even gloomier.

The only control you have over the situation is how you protect your investments from a future in which the dollar ceases to dominate global trade.

Consumer Spending Drives America and the Dollar’s Global Dominance

Over the last 200 hundred-plus years, the U.S. has climbed from its meager beginnings as a British colony to a global superpower through its robust economy, military might, and political influence. But these latter two forces are, arguably, dependent on the first, as such structures need funding to thrive.[4]

Today, the American economy is the largest in the world and maintains a tight grip on the global financial system: 80 percent of all financial transactions and 87 percent of foreign currency market transactions are made in dollars.

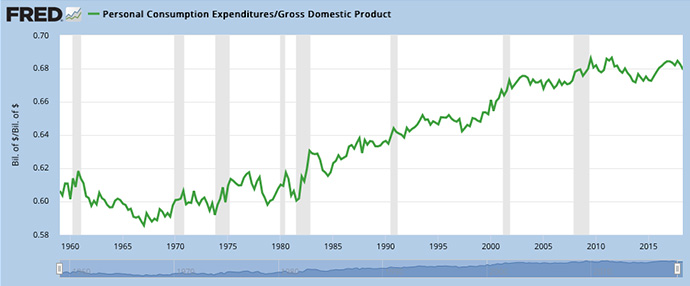

Who drives the economy? Consumers. Their spending accounts for two-thirds of GDP. It made up 68 percent of the U.S. economy in 2018.[5]

Consumer Spending/GDP. Source:Federal Reserve Bank of St. Louis

Any threat to the economy could shake the dollar’s strength and America’s hold on the financial markets.[6][7]

Used by economists as a measure to predict how likely Americans are to spend, the Consumer Confidence Index has been only gradually moving higher since July 2007.[8] This is reflected in Millennial purchasing habits, which have been compared to those of the generation who came of age during the Great Depression, the Silent Generation.

While social commentators have attributed this disturbing trend to Millennials’ ‘unique tastes and preferences,’ economists have offered more tangible reasons: despite being the most educated generation yet, they lack the wealth of all those to come before them.[9]

Millennials are less well off than members of earlier generations when they were young, with lower earnings, fewer assets, and less wealth,-Christopher Kurz, Geng Li, and Danial J. Vine of the Federal Reserve

As the largest adult generation and segment of the workforce, Millennials will be highly influential on our country’s future.[10][11] Who are they and what’s standing in their way of building the lives their parents had and continuing America’s dominance on the global stage.

Economic Disadvantages Curb Millennial Spending

The generation born between 1981 and 1996, known as Millennials, came of age during the second worse economic downturn in American history and entered the workforce at the height of globalization.[12][13] These circumstances put them at an economic disadvantage. By some experts’ accounts, they’re struggling.[14]

Globalization

The outsourcing to China and India of many middle-skilled jobs in manufacturing and other industries has left this generation with two options: low-skilled jobs or professional careers requiring inflated college degrees.[15]

Rising Cost of Higher Education

Higher education became necessary to earn livable wages, but tuition prices soared in recent years: private-school tuition skyrocketed 213 percent and public-school tuition jumped 129 percent from the 1987-1988 school year to that of 2017-2018.[16]

Student Loan Debt

Consequently, the price tag to enter the professional job market shot up. Young American’s took out student loans—a lot of them. As mentioned before, student loan debt has more than doubled since the last financial crisis and is forecast to reach $2 trillion by 2022.[17] Along with auto loans, they’re the largest component of consumer debt.[18]

Great Recession

Equipped with these pricey degrees, Millennials entered the job market when the country was in the midst of the Great Recession. Many took jobs for which they didn’t even need these credentials.[19] Others grappled with unemployment.

Both scenarios hurt the future earning potential and wealth of the most student-loan-debt-strapped generation yet. Workers who start their careers during an economic downturn can take at least 15 years to make up for the decrease in earnings they initially suffer compared to those who enter the job market during boom times.[20][21]

Worse, another downtown could be on the horizon. Read: “The Next Recession: Is a U.S. Recession Coming in 2019?”

Flat Income

Millennials are struggling… because wages are not keeping up as day-to-day costs soar–Executive Director of the Economic Hardship Reporting Project, Alissa Quart, Squeezed: Why Our Families Can’t Afford America

Generation X has a household income 11 percent higher and Baby Boomers 14 percent higher than that of Millennials, when adjusted for age and work status, wrote the authors of the previously mentioned Fed report.[22]

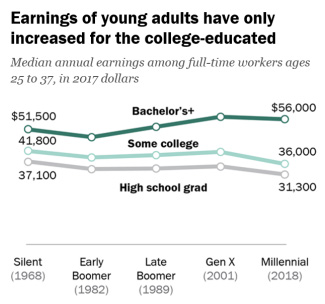

But those with college degrees are faring better than those without, reinforcing the necessity of such credentials. While degree-touting Millennials in 2018 earned the same as college-educated Gen Xers in 2001, Millennials with some college or less experienced lower earnings than their counterparts in earlier generations, found the Pew Research Center.

Slow Wage Growth across Generations. Image source: Pew Research Center

Reduced Consumer Spending

Millennials on either side of the college divide simply don’t have the spending power of the generations that came before them.

Globalization touches both groups. In spite of NAFTA and similar free trade agreements, manufacturers still can’t afford to pay U.S. wages. Professions that typically require degrees being outsourced overseas include nursing and research and development.[23]

Outsourcing has increased income inequality in the U.S., forcing many households to save instead of spend.[24]

But it’s not the only blight on young American workers’ purchasing power. Student loan debt coupled with comparatively weak wages is preventing Millennials from moving out, getting married, buying homes, and starting families—all huge drivers of consumer spending.[25] A college degree is now the second-biggest purchase an individual will make in his or her lifetime; the first is buying a home.

Debt Bombs, Rising Interest Rates, and Automation Could Kill Millennial Purchasing Power

Millennials are in a tough place economically, and it could get much, much worse for them in the coming years as they are forced to service astronomical levels of public and private debt amid the continued threats of rising interest rates and job automation.

Debt Bombs

Younger generations have a heavy load to carry into the future when it comes to public and private debt.

Public Debt

In recent years, the national debt has ballooned to more than $22 trillion. This is the highest it’s ever been and includes money the federal government must repay itself.[26]

Public debt is a portion of this number and is of particular concern because the government has interest payment obligations to bondholders. By 2020, public debt could be $16.5 trillion, estimates the nonpartisan Congressional Budget Office.

If interest rates rise back to their 30-year average of 5 percent, the federal government would have to pay $825 million a year to service that debt: half of the revenue from all personal income taxes and more than the 2018 defense budget.[27]

Private Debt

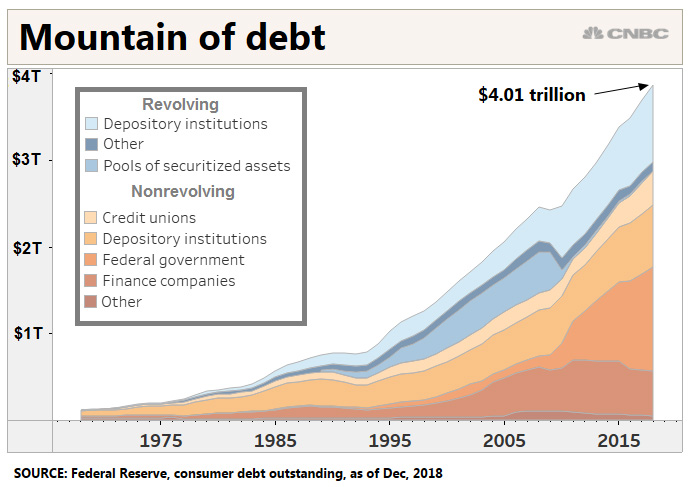

Records are also being set with private debt.

Consumer Debt

- For the first time in history, consumer debt is above $4 trillion. Credit card debt contributed $41 billion at the end of 2018 and is now at the highest level ever. Somewhat surprising considering the steep cost of borrowing: credit card interest rates are, on average, 17.41 percent, setting another record.

- Auto and student loans added another $80 billion. Consumers are now shelling out nearly 10 percent of their disposable income on nonmortgage debts.[28]

Consumer Debt Crisis

Federal Reserve, US consumer debt outstanding, as of Dec.2018. Via CNBC

Corporate Debt

- Corporate debt has far surpassed consumer debt at $9 trillion. In 2018, corporate debt as a share of GDP hit 69.3 percent; such spikes have historically signaled recessions. Worse, risky BBB-rated corporate bonds and leveraged loans comprise most of the debt.

- It’s a situation that has investors, financial regulators, and even the Fed and the IMF alarmed.[29] In April 2019, Tobias Adrian, the director of the monetary and capital markets department at the IMF, told CNBC that soaring corporate debt and loose regulations create financial market vulnerabilities that “could have a wide range of implications in the event of an economic shock.” (Read “Why the Next Financial Crisis Could Be Worse than 2008”)

Rising Interest Rates

How did private and public debt get so out of control? Historically low interest rates since the Great Recession are partly to blame. But that’s changing. Since 2008, when the Fed lowered rates to the all-time low of .25 percent, the agency has raised rates 9 times to 2.5 percent. It typically keeps them between 2 and 5 percent, but rates have shot as high as 20 percent.[30]

Higher interest rates make servicing debt more expensive. If Millennials are already so crushed by student loan debt that they’re not even moving out of their parents’ homes, just imagine the impact high interest rates could have on them.

And then there’s the rest of the debt weighing on this generation. When considering the debt collectively, higher rates could kill their spending power—not to mention trigger a domino of defaults.

Job Automation

The final blow? Job automation. A recent report by the Brookings Institute indicates automation threatens 25 percent of U.S jobs. Those who didn’t take on the massive debt of a student loan could be the worst hit: over 50 percent of jobs that don’t require a degree could disappear due to automation. Some industries are especially threatened:

- Food preparation and service (81 percent)

- Production operations (79 percent)

- Office and administrative support (60 percent).

But even bachelor’s and master’s degree holders have lost jobs to automation. Many are having to reskill to find a place in the rapidly shifting labor market.

How to Protect Your Wealth from the Demise of the Dollar

Everything you need to know to get started in Precious Metals

Learn how precious metals can strengthen your portfolio, protect your assets and leverage inflation.

Request the Free GuideWill economically disadvantaged and debt-burdened younger generations be able to sustain America’s global economic might in the years to come?

While that remains to be seen, one thing is certain: they have many forces weighing on their prosperity and purchasing power. And, if consumer spending tanks so could the GDP. Declining economic productivity can devalue our nation’s currency. With Russia and China already actively working to undermine the dollar, how much more would it take to dethrone its coveted position as the global reserve currency?

In this environment of economic uncertainty, the only control you have is over how you protect your own wealth.

Examining the actions of countries, central banks, and smart money can offer some guidance. They’ve all been moving into physical precious metals.

If you’re thinking about your financial future 10 years down the road or more, consider following suit. Gold and silver coins are the investment for the decade.