Eric Sepanek

SBC Founder

Eric Sepanek is the founder of Scottsdale Bullion & Coin, established in 2011. With extensive experience in the precious metals industry, he is dedicated to educating Americans on the wealth preservation power of gold and silver.

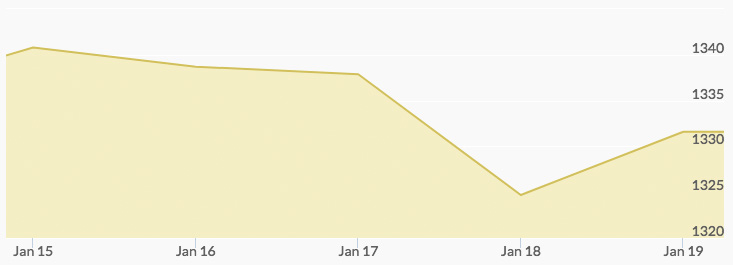

Markets were closed Monday for the Martin Luther King, Jr. holiday. Tuesday’s open saw gold prices pullback slightly from the previous week’s close to $1,335.31 but then rallied to close the day at $1,340.92, its highest close since September 2017. On Wednesday morning, the price of gold slipped to $1,336.17 and continued to soften until the close at $1,328.70. The yellow metal then pushed up to Thursday’s open at $1,329.75 before pulling back slightly to close at $1,327.95. Friday kept the pattern of bullish recovery seen in recent months to close out the week: markets opened up significantly at $1,334.72 and then settled to $1,331.84 to close out the week.

Tuesday’s trading was dominated by news of an additional dollar crash, as the Bloomberg Dollar Index approached its lowest level in three years. 1 The news capped five straight weeks of declines and although the greenback showed some signs of recovering in Tuesday’s trading, reports underline that the trend of a weakening dollar and a bull market for gold continues. 2

Wednesday bore witness to another Bitcoin crash, as the cryptocurrency shed approximately a quarter of its value due to concerns about a regulatory crackdown on trading of cryptocurrencies. 3 South Korea’s finance minister Kim Dong-Yeon said Wednesday that shutting down cryptocurrency trading in the country was ‘still one of the valid options on the table,’ which sent markets into freefall.

To end the week, gold market watchers were treated to a report on Thursday that, despite its recent rise, gold still has plenty more room to run. The report found that while this week saw a slowdown in the gold rally, core market fundamentals remain bullish. Additionally, market sentiment among options traders appears to exhibit a strong bullish trend, and even from a seasonality perspective, gold historically seems to do especially well in January and February.