Eric Sepanek

SBC Founder

Eric Sepanek is the founder of Scottsdale Bullion & Coin, established in 2011. With extensive experience in the precious metals industry, he is dedicated to educating Americans on the wealth preservation power of gold and silver.

Add SBC on Google as a preferred source to see more market related news like this when you search.

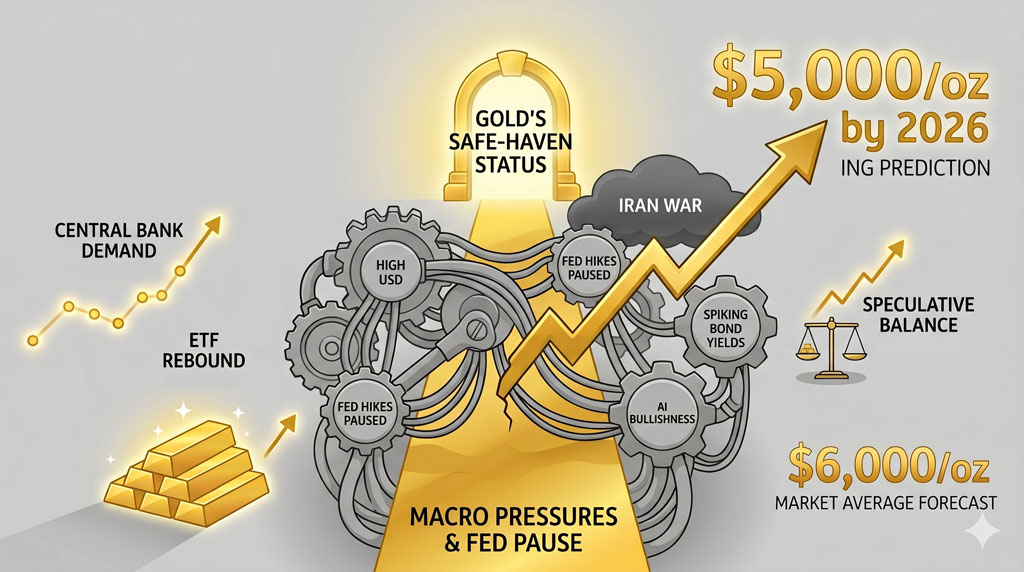

Many investors have been stumped by gold’s muted performance over the past few months, especially in light of the Iran War.

Many investors have been stumped by gold’s muted performance over the past few months, especially in light of the Iran War.

The yellow metal has a long-held reputation for thriving during bouts of geopolitical upheaval. Yet, since the outbreak of the conflict in the Middle East, gold has remained relatively flat.

This seemingly contradictory trend has puzzled markets, leading to a critical question: Is gold losing its safe-haven status, or are traditional patterns temporarily interrupted by other powerful forces?

Gold’s Rapid Rise & Quick Sputter

Gold prices kicked off the year on a high note, spiking to an all-time high in January. However, that impressive momentum has waned over the past few months. When the Iran War broke out in late February, historical charts would have strongly indicated a rebound in price action.

For decades, the yellow metal has shown a clear pattern of strengthening during periods of economic and geopolitical instability. Since the war’s onset, though, gold has uncharacteristically receded by about 12%.

Recently, ING addressed this central issue in a revealing report, suggesting that gold’s current weakness is a result of macroeconomic and political forces rather than tepid demand or a systemic change in the precious metal’s appeal.

Why This Crisis is Different

According to ING analysts, this crisis stands in stark contrast to previous events. In the past, the fuel that propelled growth in safe-haven and commodity markets usually consisted of:

- Weak economic growth

- Federal Reserve rate cuts

- Stressed financial markets

- Softening U.S. dollar

- Falling real interest rates

In virtually every category, the Iran War has created opposing conditions. The Strait of Hormuz, which has become a focal point in the conflict, controls 20% of the world’s oil supply. This has catapulted energy prices, resulting in:

- A stronger USD due to its key role in the petrodollar system

- Lower expectations for rate cuts as the Fed waits to assess the full economic impact

- Higher bond yields as investors demand greater returns to offset inflation

At the same time, the stock market remains unbothered, charting new highs consistently, partially explained by AI bullishness. These factors tend to keep downward pressure on gold prices.

The Parallel With the Russian-Ukraine War

Analysts at ING point to gold’s trajectory in the wake of Russia’s invasion of Ukraine as a useful comparison. Immediately following the attack, gold popped initially before giving way to spiking energy costs, Fed uncertainty, and a dual rise in USD and yields. A similar cycle is playing out right now, albeit in a shorter period. The silver lining for gold investors is that this faster market rotation could mean a rebound in gold prices is reached more quickly.

Interest Rates Stand as Gold’s Biggest Hurdle

Amid all the variables currently working against gold, ING underlines the Fed’s pausing of rate cuts as the largest obstacle. With rates remaining elevated, investors remain exposed to yield-bearing assets. These securities lose their appeal when rates are lower, creating a concomitant rise in demand for non-yielding assets, such as gold. In turn, these comparatively higher rates boost the dollar’s value, further weighing on gold’s performance.

In the latest Fed meeting in April, rates remained unchanged, and Federal Reserve Chair Jerome Powell struck a cautious tone due to the uncertainty caused by Middle East tensions. The combination of a robust job market, with unemployment at 4.3%, and a stubborn inflation rate of 3.8%, minimizes the urgency for rate cuts.

The Bullish Signals Hiding Beneath Gold’s Pullback

In addition to historical comparisons, ING highlights underlying demand and bullish market trends to indicate that gold’s upward movement is paused, rather than reversing:

Robust Central Bank Demand

Central banks, the largest purchasers of physical metal, accumulated 27 tons in Q1 2026, marking a 17% increase from the previous quarter. This follows a record total gold demand of 5,000 tons in 2025. Furthermore, the People’s Bank of China notched its 15th straight month of gold buying, extending the country’s reserves to 2,305 tonnes — one of the fastest-growing gold stockpiles in the world.

Exchange-Traded Funds Rebound

Gold exchange-traded funds (ETFs) shattered records at the start of 2026, and the retail buying spree continues. In April, global gold ETFs recorded $6.6 billion worth of inflows, with Europe leading the pack. Despite this recent rise in activity, ING analysts indicate there’s plenty more room to run as ETF holdings remain far below highs reached in November 2020.

Speculative Positioning Remains Low

Another bullish signal from the gold market is a lack of speculative buying. When futures positioning reaches crowded territory, the higher risk can signal a potential reversal. Even with prices sitting near record levels, gold futures buying remains balanced. This points to a healthy market without overleveraged investments or unfounded euphoria.

Gold’s Safe-Haven Status Remains Intact

The main takeaway from ING’s timely report is that gold’s safe-haven status remains unchanged. Zooming in on the metal’s short-term moves within a tight timeframe risks overlooking over a century of performance, which confirms gold’s tendency to keep pace with inflation by rising when the broader market stumbles.

The temporary climate of dollar strength, stagnant rate cuts, equity growth, and steady bond yields doesn’t negate the foundation of gold’s long-term value, proven by relentless central bank demand and historical data. ING expects gold to quickly rebound once these macroeconomic pressures are lifted.

By the end of 2026, ING analysts project prices to hit $5,000/oz. Despite the group’s overall bullishness, this target actually falls below the market average. According to our 2026 gold price forecast analysis, experts across the economic, precious metals, and investment spheres believe gold is likely to reach $6,000/oz before the year’s end.