John Karow

Precious Metals Advisor

John Karow is an experienced lawyer and Precious Metals Advisor at Scottsdale Bullion & Coin. He holds degrees from Lehigh University, the University of Missouri, Cornell University, and St. John’s University School of Law. John is a knowledgeable authority in precious metals, dedicated to helping clients navigate economic cycles and gold and silver investments.

Eric Sepanek

SBC Founder

Eric Sepanek is the founder of Scottsdale Bullion & Coin, established in 2011. With extensive experience in the precious metals industry, he is dedicated to educating Americans on the wealth preservation power of gold and silver.

Gold’s relentless rally saw the precious metal surge nearly 10% just a week after breaking the $4,000/oz mark. At the same time, prominent voices in finance and media are breaking from decades of convention to question the stability of US assets.

In this week’s The Gold Spot, Scottsdale Bullion & Coin Founder Eric Sepanek and Precious Metals Advisor John Karow discuss what gold’s sustained strength signals about the US dollar and Treasuries, what the recent pullback suggests about the metal’s next moves, and why even long-time skeptics are beginning to recognize gold’s growing central role in global markets.

Gold’s Post $4,000/oz Moves

About a week ago, gold prices blew through $4,000/oz, putting to rest questions about the precious metal’s momentum. Within a week, spot prices nearly tacked on another 10% gain, stretching to $4,380.89/oz before a minor sell-off. Gold prices remain above the $4,000/oz threshold, signaling a new floor to support its price discovery.

The yellow metal’s boom is exciting for precious metals investors and a further indication of the asset’s inherent value, but this robust price action casts a shadow on US assets more broadly. Generally speaking, gold and USD-linked instruments — such as the dollar and government bonds — move inversely.

This market-wide phenomenon is playing out right now as record-high gold prices reflect structural weakness in US assets.

What Gold’s Strength Means for US Assets

Gold’s rapid ascent may seem overheated, but it’s less a warning sign for the metal itself and more a reflection of investors shifting out of paper gold instruments and into physical gold. The yellow precious metal has already climbed by more than 50% in 2025 — far above the 10% to 15% gains typically seen in a stable economic environment.

Meanwhile, the US Bond Index plunged 10% early in the year and has yet to recover. With the Federal Reserve resuming rate cuts, the resulting lower yields on long-term bonds continue to weigh on demand.

“The minute we start dropping interest rates, that’s going to devalue bonds. Other countries holding Treasuries will start selling those to buy physical assets like gold and silver.”

Eric Sepanek

SBC Founder

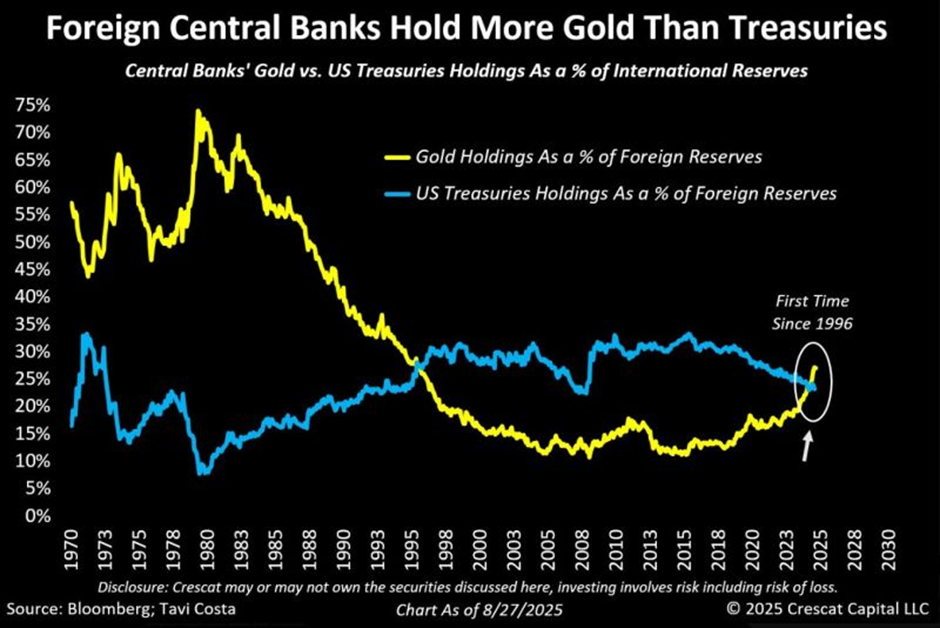

The US dollar also faces a sharp drop in global demand, particularly from official foreign investors. Nations deliberately pursue de-dollarization to reduce exposure to the US economy as national debt mounts, which just hit $38 trillion, and concerns over dollar-based risks grow. For the first time in years, central banks are buying more gold than dollars.

Source: Crescat Capital LLC via Investing.com

Major Media & Financial Names Change Tune

For decades, major media outlets and leading financial institutions have advocated the 60/40 investment strategy, which allocates 60% of funds to stocks and 40% to government bonds. Recently, some of the most recognized — and least expected — leading names have revised that conventional approach, opting for a more gold-heavy alternative.

Currently, many significant names are pushing for a 60/20/20 portfolio strategy, in which investors allocate 60% to stocks, 20% to bonds, and 20% to gold. CNBC, Bank of America, Morgan Stanley, Peter Schiff, and a growing chorus of financial leaders and media moguls are changing their tune on bonds and gold.

This is a tacit acknowledgement that US Treasuries no longer provide the financial stability to justify their inclusion as a bedrock of investment portfolios.

Gold Now Considered Safe-Haven

Gold’s exclusion from the traditional 60/40 strategy reflected widespread skepticism among conventional investment firms. The past few years have shattered this dominant belief system as bond markets dip, the US’s credit rating falters, national debt spikes, and the greenback sputters.

Simultaneously, gold is reclaiming its position as a cornerstone of the global economy. Since the end of the gold standard, countries have nominally attached their fiat currencies to the physical metal through massive gold reserves. Now, the yellow metal is taking a more official central position. Recently, the global banking system recognized gold as a Tier 1 asset, on par with bonds and the dollar.

“Treasury bonds are no longer low risk, and that’s a reflection of the massive debt load the world is carrying.”

John Karow

Precious Metals Advisor

Financial Heavyweights Signal Confidence in $5,000 Gold

Even after briefly pulling back from its almost $4,400/oz peak, many analysts and institutions believe gold’s rally is far from over. Major financial players are still calling for record-breaking highs ahead. Bank of America and Société Générale, and now JP Morgan project gold reaching $5,000/oz by 2026, while HSBC predicts the ongoing “bull wave” could carry prices to that level within that timeframe.

Jim Thorne, Chief Market Strategist at Wellington-Altus, expects gold to reach $5,000/oz, arguing that the metal is in the midst of a historic breakout fueled by weakening confidence in US fiscal management. Rob McEwen, CEO of McEwen Mining, echoes that view, linking rising public and private debt to what he believes is a solid setup for gold to climb to $5,000/oz.

James Luke, Metals Fund Manager at Schroders, calls that same price “frankly conservative,” noting that macroeconomic imbalances and persistent inflation could push gold even higher. The deVere Group forecasts $5,000/oz in the near to medium-term, citing inflation, geopolitical risks, and sustained investor demand.

Wall Street heavyweight Jamie Dimon of J.P. Morgan went even further, saying gold “could easily go to $5,000 or $10,000 in environments like this,” referring to today’s mix of fiscal strain and inflationary pressure. Similarly, BlackRock’s Evy Hambro recently commented that gold could “go a lot higher” as investors increasingly turn to it amid global uncertainty.

It’s evident that a rising number of prominent names believe $5,000/oz gold and higher is on the table.

Buy the Dip in Gold and Silver

Gold’s recent 5% pullback doesn’t seem so extreme when viewed in the broader context. The yellow metal has been on a historic rally, posting gains of more than 50% in less than a year. Zoom out to two years, and the gains are over 100%. No healthy asset can achieve those returns without a breather from time to time.

With leading media and financial figures encouraging investors to invest more in gold and silver, central banks topping up their reserves, and gold and silver price forecasts continuing to rise, the outlook for the precious metals market is bullish. These short-term dips should be viewed as a prime opportunity for investors to dollar cost average into a lower cost basis.

People who buy physical gold are long-term players. This is the classic buy-the-dip pattern. When the iron’s hot — strike.–

Peter Schiff warns of a category-5 financial hurricane that could supercharge the gold and silver rally, so investors shouldn’t wait around until conditions are too bad. UBS analysts recently advised investors to use short-term dips to augment their gold and silver exposure. As the old saying goes: It’s better to buy gold and wait than to wait to buy gold.

👉 Ready to make smarter moves in the precious metals market? Unlock the 22 critical errors to avoid when buying precious metals with our free Precious Metals Investor Guide.

Handpicked Related Articles & Videos

Question or Comments?

If you have any questions about today’s topics or want to see us discuss something specific in a future The Gold Spot episode, please add them here.

Comment

Questions or Comments?

"*" indicates required fields