Todd Graf

Precious Metals Advisor

Todd Graf is a seasoned Precious Metals Advisor at Scottsdale Bullion & Coin. He has a decade-long career in finance, previously at Morgan Stanley and Vanguard. He is Series 7 licensed and has extensive experience in traditional and defensive assets, providing clients with solid investment strategies.

Joe Elkjer

Precious Metals Advisor

Joe Elkjer, a Precious Metals Advisor at Scottsdale Bullion & Coin since 2019, specializes in helping clients protect their assets through tangible investments. With a strong background in business and finance, he emphasizes stellar customer service and stays dedicated to informing clients about market impacts through frequent appearances on The Gold Spot.

A potential shakeup at the Fed is sending shockwaves through markets and raising new questions about the dollar’s future.

Watch this week’s The Gold Spot to hear Scottsdale Bullion & Coin’s Precious Metals Advisors Joe Elkjer and Todd Graf unpack Warsh’s nomination, what this could mean for interest rate policy moving forward, and how this impacts gold’s outlook.

Trump’s Fed Chair Nominee Fails to Calm Fears

The Federal Reserve has been under pressure from President Donald Trump for years to lower interest rates. The weight of POTUS’s ire has fallen squarely on the shoulders of Fed Chair Jerome Powell, who was ironically appointed by Trump during his first term. A prolonged macroeconomic climate dominated by stubborn inflation, trade uncertainty, and geopolitical risk has drastically slowed rate cut expectations.

Although Powell is expected to last until his term ends on May 15, 2026, many worry that the Fed’s credibility crisis — driven by political influence over what’s meant to be an apolitical institution — could further weaken the U.S. dollar. Powell, who received bipartisan support during the president’s attacks, is expected to be replaced by Kevin Warsh, whom some fear may have a political bent rather than an unbiased eye on the market.

Despite serving on the Federal Reserve Board of Governors from 2006 to 2011, Warsh’s future decision-making remains uncertain, with President Trump’s preference for lower rates looming in the background. During his recent April 2026 confirmation hearing, Warsh emphasized that “Fed independence means everything to me,” and that he would not pre-commit to any rate decisions.

Market Reaction Signals Policy Uncertainty

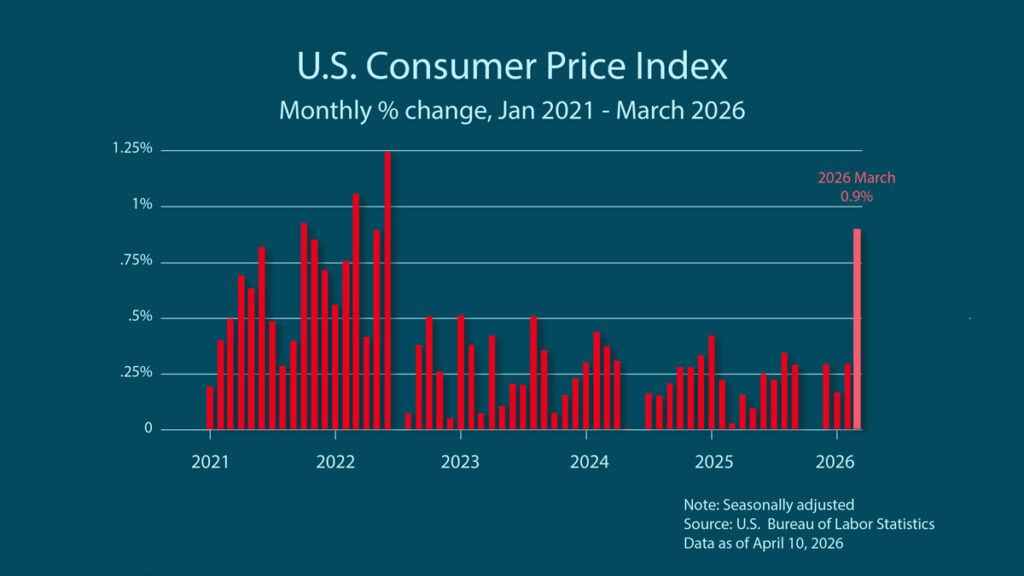

Markets sent mixed signals throughout Warsh’s testimony, reflecting rising uncertainty around the Fed’s rate-cut outlook. Equities weakened during and after the hearing, while oil prices moved higher following shaky peace talks between the U.S. and Iran. This uneven reaction to a potential leadership shift at the Fed mirrors broader tensions in an already strained macroeconomic environment.

Warsh’s earlier justification for rate cuts rested on the anticipated economic boost from artificial intelligence — an outlook dependent on disinflationary growth. However, rising energy prices tied to geopolitical instability have complicated that narrative, reinforcing inflationary pressures even as growth expectations remain in flux.

With Q4 2025 GDP revised to 0.7%, the Fed now faces a difficult balancing act between modest growth and persistent inflation. This tension complicates the path forward for interest rates, adding another layer of uncertainty for investors.

What Fed Chair Nominee Kevin Warsh Means for Gold Investors

Warsh’s nomination to lead the Federal Reserve presents a seemingly contradictory scenario. During his tenure as a Fed Governor, Warsh openly criticized quantitative easing (QE) and pushed to limit the Fed’s injection of liquidity into the system, driven by a tighter balance sheet. However, critics draw a straight line between Warsh’s uncharacteristic shift toward championing rate cuts and Trump’s return to the White House.

For gold investors, this policy conflict can result in two possible outcomes:

- 📉 A hawkish Kevin Warsh hesitates to cut rates, supporting a stronger U.S. dollar and pressuring gold prices in the near-term.

- 📈 A politically aligned Kevin Warsh cuts rates at Trump’s behest, lowering interest rates and weakening the U.S. dollar, raising gold’s appeal.

The fact that nobody can predict the outcome reveals the pervasive uncertainty within the market. In these fiscally ambiguous environments, gold emerges as a strong option given its ability to keep pace with inflation.

“Either way, the uncertainty itself is a reason to hold gold.”

Todd Graf

Precious Metals Advisor

The Fed’s Gradual Devaluation of the Dollar

The fight over fiscal policy and interest rates is taking place against a backdrop of skyrocketing national debt, persistent federal deficits, and ballooning interest payments. Clearly, interest rates are a symptom of a larger problem of dollar devaluation.

In the Wall Street Journal, Judy Shelton highlights how the Fed has effectively overseen a targeted 2% annual decline in the dollar’s purchasing power since 2012, under the banner of “price stability.” However, this stability has looked more like deterioration, with the dollar losing about 80% of its value over the lifespan of the average American.

In reality, inflation has set in at a much more rapid pace, with the dollar slipping 3.31% on average per year since 1980, per Minneapolis Federal Reserve data. Since Jerome Powell took over in 2018, cumulative inflation has resulted in a 31% price increase in the span of eight years. In the past few years alone, prices have risen at a faster pace than the Fed’s targeted 2%.

Monetary Policy Can’t Fix a Fiscal Problem

Kevin Warsh has signaled a desire to shrink the Fed’s $6.7 trillion balance sheet, effectively pulling liquidity out of the financial system and tightening financial conditions. Theoretically, this fiscal discipline, which stands in stark contrast to the Fed’s embrace of Modern Monetary Theory, would prop up the dollar.

However, the fiscal policy of the U.S. central bank isn’t the root of the issue. The Constitution places the power of the purse with Congress, which is responsible for setting budgets. With Congress refusing to rein in spending, the Fed cannot meaningfully stop the runaway train of inflation or dollar devaluation.

“You cannot shrink the balance sheet while Congress keeps running the same deficits that built it. It's simply not mathematically possible.”

Todd Graf

Precious Metals Advisor

Gold’s Story Doesn’t Begin or End With Warsh

The political furor that has arisen around President Trump’s pressure on the Fed’s independence and Kevin Warsh’s nomination has stolen headlines and captivated investors, but this event is a minor influence on the gold market when viewed from a bird’s-eye view. In the short term, gold prices retreated about 13% from all-time highs within days of the Fed Chair nominee’s confirmation hearing.

However, prices swiftly recovered to around $4,800/oz and remain up nearly 200% over the past two years. Besides, gold fell before it soared in 2008, leaving many wondering if it’s gearing up to do the same now. While short-term moves are dominated by immediate market sentiment, the long-term trajectory is fueled by sustained drivers, such as dollar erosion, central bank demand, de-dollarization, deficit spending, and geopolitical instability.

Gold Goes Digital, But the Fundamentals Remain

![]()

The World Gold Council (WGC) recently announced a new initiative, dubbed “Gold as a Service,” which is aimed at bringing gold further into the modern financial system. In partnership with Boston Consulting Group, the plan introduces standardized digital infrastructure that enables physical gold to be traded, tracked, and even used as collateral more easily. In simple terms, it’s about turning gold from a static asset sitting in a vault into something more dynamic and deployable within financial markets.

This move reflects the global financial system’s recent recognition of gold as a Tier 1 asset, placing it on equal footing with the dollar and U.S. Treasuries in terms of debt issuance. These moves only enhance the utility and accessibility, and therefore, the demand, for gold without undermining its foundational appeal as an inherently valuable, physical, inflation-resistant asset.

“Our take is simple: Physical allocated gold remains the foundation. Digital infrastructure makes gold more accessible to more investors. That's more demand for the same finite supply.”

Joe Elkjer

Precious Metals Advisor

If these developments are raising questions about your own strategy, download a FREE copy of our in-depth Precious Metals Investment Guide. It covers everything you need to know about buying gold and how it can help protect your wealth in an increasingly uncertain fiscal environment.

Question or Comments?

If you have any questions about today’s topics or want to see us discuss something specific in a future The Gold Spot episode, please add them here.

Comment

Questions or Comments?

"*" indicates required fields